The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Chartered accountant Michael Brown is the founder and CEO of Double Entry Bookkeeping. He has worked as an accountant and consultant for more than 25 years and has built financial models for all types of industries.

Step 3 – Divide costs by equivalent units

In our next section, we will do a comparison and reconciliation of the same number of products through one process with each of the two methods. Notice that by including the costs brought forward, 100% of the cost of producing the units in beginning WIP are included. The units that remain in the ending work-in-process inventory, however, are not complete.

2 Equivalent Units (Weighted Average)

We calculated total equivalent units of 11,000 units for materials and 9,800 for conversion. The 750 shells in production at the end of January were 60% complete as to conversion costs and 100% complete as to direct materials, so in February they will need 40% more conversion but 0% more direct materials. Process costing is used to figure out how much it costs to produce items that are very similar or identical, like chocolate bars or cans of soda.

Step Two: Computing the Equivalent Units of Production

Conversion costs are those costs incurred to convert raw materials into the final product (meaning, direct labor and overhead). FIFO (First-In, First-Out) and WA (Weighted-Average) are methods used to assign costs to units produced. FIFO assumes that the oldest costs are assigned to the units completed first. For example, for a factory is making chocolate bars, FIFO means the cost of the ingredients and labor from the beginning of the production period are used first to calculate the cost of the finished bars. This helps to track the flow of costs more accurately based on the production timeline. On the other hand, the Weighted-Average method blends all the costs together to find an average cost per unit.

How confident are you in your long term financial plan?

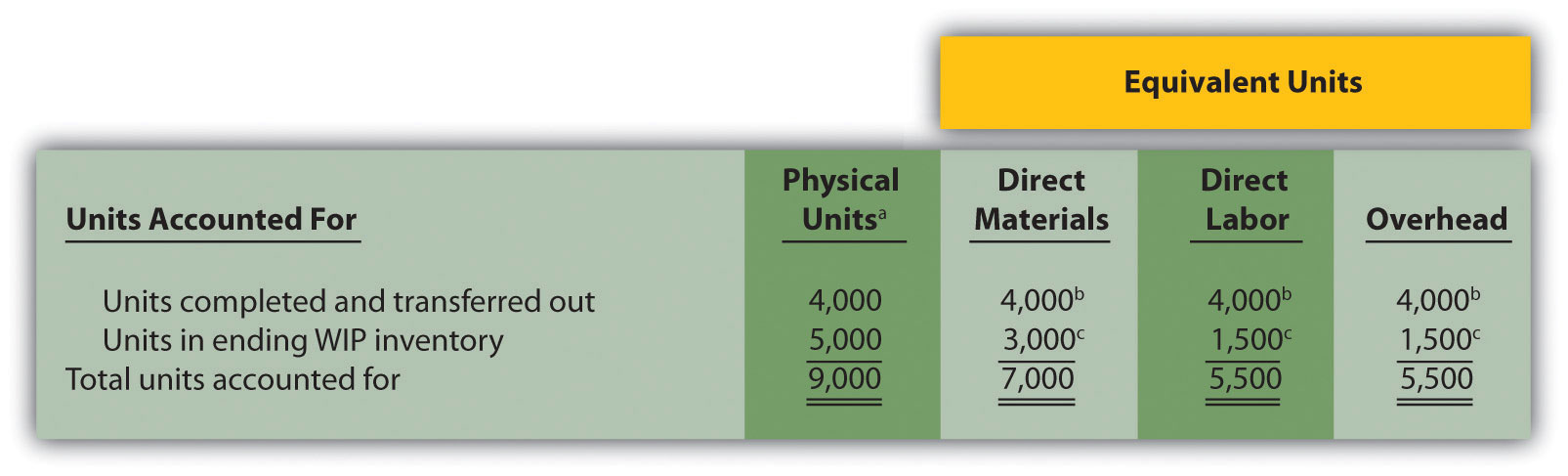

Any units that have been moved into process 2, will be subtracted from the WIP inventory for process 1. For total equivalent units, this is the sum of the units transferred out, with your ending inventory. The cost of each element (i.e., the difference between depreciation on the income statement and balance sheet material, labor, and overhead) is divided by the equivalent units of production of that element. Under the weighted average method, costs transferred in from last month are added to this month’s costs and distributed across all units.

- First, we need to know our total costs for the period (or total costs to account for) by adding beginning work in process costs to the costs incurred or added this period.

- The units that were completed and transferred out plus the ending inventory equal the total units to account for.

- This is called the Weighted Average method and there are other methods too (discussed below).

- In this method, both the beginning and ending inventory is converted into equivalent units, so there is a bit more work to do.

- The equivalent unit cost of materials is, therefore, $1.31 ($118,000/90,000 EU).

Therefore, the started and completed unit of 75,000 units was computed by deducting the ending WIP (5,000 units) and beginning WIP (10,000 units) from the total units to account for of 90,000 units. Thirdly, the equivalent units of production for the closing work-in-progress should be determined by considering the number of units of closing work-in-progress and the level of completed work. To solve the problem of work-in-progress, we can calculate equivalent units of production (or “effective production”). The output of a department is always stated in terms of equivalent units of production. The shaping department completed 7,500 units and transferred them to the testing and sorting department. No units were lost to spoilage, which consists of any units that are not fit for sale due to breakage or other imperfections.

Determining equivalent units are important in determining total units of production, but it also influences cost allocation decisions in manufacturing processes. In this article, you will see the comparison between FIFO and weighted average, with an easy to understand example. We will calculate a cost per equivalent unit for each cost element (direct materials and conversion costs (or direct labor and overhead).

The 1,750 ending WIP units are 100% complete with regard to material and have 1,750 (1,750 × 100%) equivalent units for material. The 1,750 ending WIP units are only 40% complete with regard to conversion costs and represent 700 (1,750 × 40%) equivalent units. The total materials costs for the period (including any beginning inventory costs) are computed and divided by the equivalent units for materials.